CBDCs vs. Crypto: Why They're Not the Same Thing

A clear-eyed look at why the digital currencies central banks build are structurally the opposite of the cryptocurrencies they claim to mirror.

By the time that cryptocurrency was less an oddity and more a global movement — around when Bitcoin's market cap had passed first some of the largest banks in the world and stablecoins began settling trillions annually — traditional finance did not unleash their enthusiasm. An anxiety, then a mimicry, then a very specific kind of step that made something that at its distance looked like crypto and up close not in the slightest. Сentral banks around the globe began working on their own version of what they would term Central Bank Digital Currencies and the sales pitch was that they could deliver everything crypto advocates claimed they wanted — the speed and efficiency, digital convenience, programmable money — without all of those dastardly decentralization drawbacks.

So effective was the pitch that a substantial chunk of the financial press began to speak about CBDCs as "central bank crypto" or "government-backed digital currency," phrasing which implies an affinity between the two, at a level that doesn't actually exist. The technical implementations are different. The governance is different. The incentive structures are different. And, most crucially of all — who is in control over what you do with your money answer to this question has the exact opposite. Crypto distributes that control. CBDCs have the potential to concentrate it more completely than any other form of money has ever been able to.

This is not an accident, nor an externality. That is literally the whole point of the design. Neither politicians, finance ministers nor law enforcement agencies took a look at Bitcoin and said this world needs more financial freedom. And their conclusion was that the world needed an answer to it — one that could match superficial features like speed and digital convenience while keeping, at least in some form, all of the oversight physical cash and traditional bank deposits were beginning to lose. CBDCs are the answer, and distinguishing between CBDCs and the cryptocurrencies they were created to replace is one of this decade's more consequential financial literacy questions.

Where the Idea Originated

The most recent CBDC to successfully deploy was the Bahamas Sand Dollar, originally a digital version of the Bahamian dollar released in October 2020 by the Central Bank of the Bahamas to facilitate financial inclusion over an archipelago not particularly accommodating to brick-and-mortar banks. The Sand Dollar experienced some uptake and showed that retail CBDC technical infrastructure is still possible in limited jurisdictions without some sort of catastrophe. The eNaira was November 2020 when Nigeria set to launch as the first major economy with a CBDC so this comes in at Number two With regards to adoption, the eNaira's trail has been noteworthy. After a year of more, less than one percent of Nigerians had used it.

The most significant CBDC initiative to date is, by all reasonable standards, China's e-CNY (also known as Digital Currency Electronic Payment depending on which governmental document you refer to). Research at the People's Bank of China in 2014 and pilots rolling out across a few cities into 2019-2020 before you got this major push during the Beijing Winter Olympics of February 2022 when foreign visitors were able to accept to use e-CNY on-site in some venues, on transit or retail. But the absolute figures of transaction volumes — trillions of yuan in cumulative throughput by 2025 — was still disputed among academia as a lion's share came through organic uptake or governmental-distributed promotional payments? There is no argument about the e-CNY being the biggest operationally functional retail CBDC in any major economy with other central banks looking at it carefully as a reference design.

In 2023, the European Central Bank moved to take preparatory steps towards its own less invasive digital currency, with technical design and stakeholder consultations slated between now and 2025. Tentative timeline: late 2020s, subject to legislative approval that isn't yet secured. And leverage an explored digital pound from the Bank of England. India launched its digital rupee in pilot phase in December 2022. Starting in 2023 Russia also began testing the digital ruble. The DREX project in Brazil, which stands for direct resource exchange, has undergone broad-level testing since 2024. More than 130 countries — approximately 98% of the world’s GDP — are now researching, developing or piloting some form of CBDC according to the Atlantic Council's CBDC tracker, with three currencies fully launched, dozens less advanced in pilot and others only at early design stages.

The bulk of the technical infrastructure for these projects is not really blockchain in the decentralized sense. The majority of the CBDCs implemented adopt a centralized or permissioned ledger technology solution — the central bank, or a select group of authorized intermediaries, runs the network and confirms transactions while holding on to and providing access to validated canonical records of transaction data. In other words, because the central bank is the consensus measure (there is no need for a consensus mechanism in the cryptocurrency sense). The "digital" in CBDC is a reference to the form factor, not some architectural analogue to decentralized cryptocurrency.

Caveat in the Small Print

The key structural element differentiating CBDCs from cryptocurrencies and physical cash is not their digital form. Central banks called it "programmability" in their technical documentation, and their critics call it plainly something like "controlling how you can use your own money."

A CBDC, if properly designed, may be programmable in ways that traditional money never could. This may include an expiry — funds that need to be utilized prior to a specific point in time or else returned to the issuer. It may also have geographic limitations — such as funds that operate only in specific jurisdictions or zip codes. It may carry spending category restrictions — money that can be used for groceries but not gasoline, or for child care but not entertainment. It can have time-of-day restrictions, demographic restrictions, or just any rule that the authority of the issuing value decides to set up at protocol level. All of these features are theoretical. These have been recorded in central bank working papers and even evidenced, on occasion, through pilot programs. There are actually programmability provisions in the eNaira specification for situations like this. The e-CNY does as well. This is discussed explicitly in the digital euro design documents, with an array of reassurances about responsible use of such an option.

Thus, the ideals from advocates of CBDC is that programmability is a feature not a bug — programmable money allows for greater welfare targeting, more effective monetary policy stimulus (both space and size), quicker response to economic conditions. Opponents of a CBDC would argue that any infrastructure which could provide those benefits could also enable every method of financial coercion actionable by an authoritarian or just simplistic government; and that the history regarding the behavior of governments with the technological capability for surveillance and censorship is one such that if there are enough political incentives to do so, watching, silencing, deporting or enslaving dissenters will eventually be tried. In jurisdictions where currency restrictions and capital controls are already a well-established policy tool, this is not a theoretical concern.

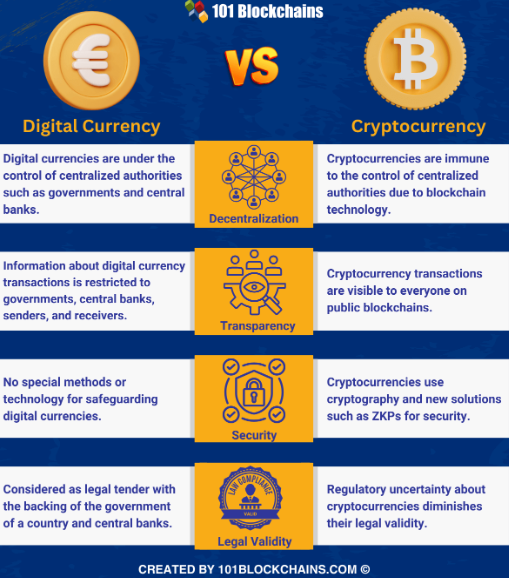

Yet the concern extends to the dimension of privacy. Inherently, any transaction in a CBDC is completely transparent to the issuing central bank and any governmental agency it chooses to share data with. From the perspective of the central bank cash transactions are anonymous. Bank deposits are also public — the government (but not a single central authority unless the bank flags them) can see what you deposit in banks as well. Note that cryptocurrency transactions are pseudonymous (visible to all from a public ledger, but not tied directly to an identity without further external linkage). CBDC transactions bring financial transparency to one line of sight only ever since the rise of monetary technologies. The claim that "if you have nothing to hide, you have nothing to fear" is the argument that has always come before every increase of state power into private life (and the money side of your existence is one of the most consequential ranges this argument can be used against).

Result in the real world vs. the Crypto response

The reaction of the cryptocurrency community to the development of CBDCs has been mostly negative, and it has been better articulated than mainstream finance commentary because its authors have an understanding of the technical landscape that most politicians and most journalists lack. The basic point is that they are not comparable; a CBDC and a cryptocurrency can both be digital and involve cryptographic signatures, but so what? They differ in the control over issuance and freezing of accounts, delegation of programming restrictions, transaction reversal or access to the transaction graph. In all those dimensions, a CBDC is more akin to a bank account than Bitcoin, and the implementation of CBDC at the central bank level is more like that of a credit card network than a peer-to-peer settlement protocol.

So far the real-world data has tended to give a nod towards scepticism. The eNaira, despite mandates and incentives, has not been widely embraced precisely because ordinary citizens, when given a choice, will prefer instruments they understand and trust over those constantly sold to them by the government. So far, on the adoption metrics for China's e-CNY, they're not really in favour of the CBDC — at least where crypto and CBDCs can compete freely; the use of stablecoins for cross border commerce has been successfully continuing (and in many instances expanded!), notwithstanding official disapproval even inside China. In the US, President Trump signed an executive order in January 2025. The order incarnated a particular ideological position, but it also embodied a calculation that the political costs of a US CBDC exceed its hypothetical benefits — not a calculation confined to any single administration and one made across party lines in various forms.

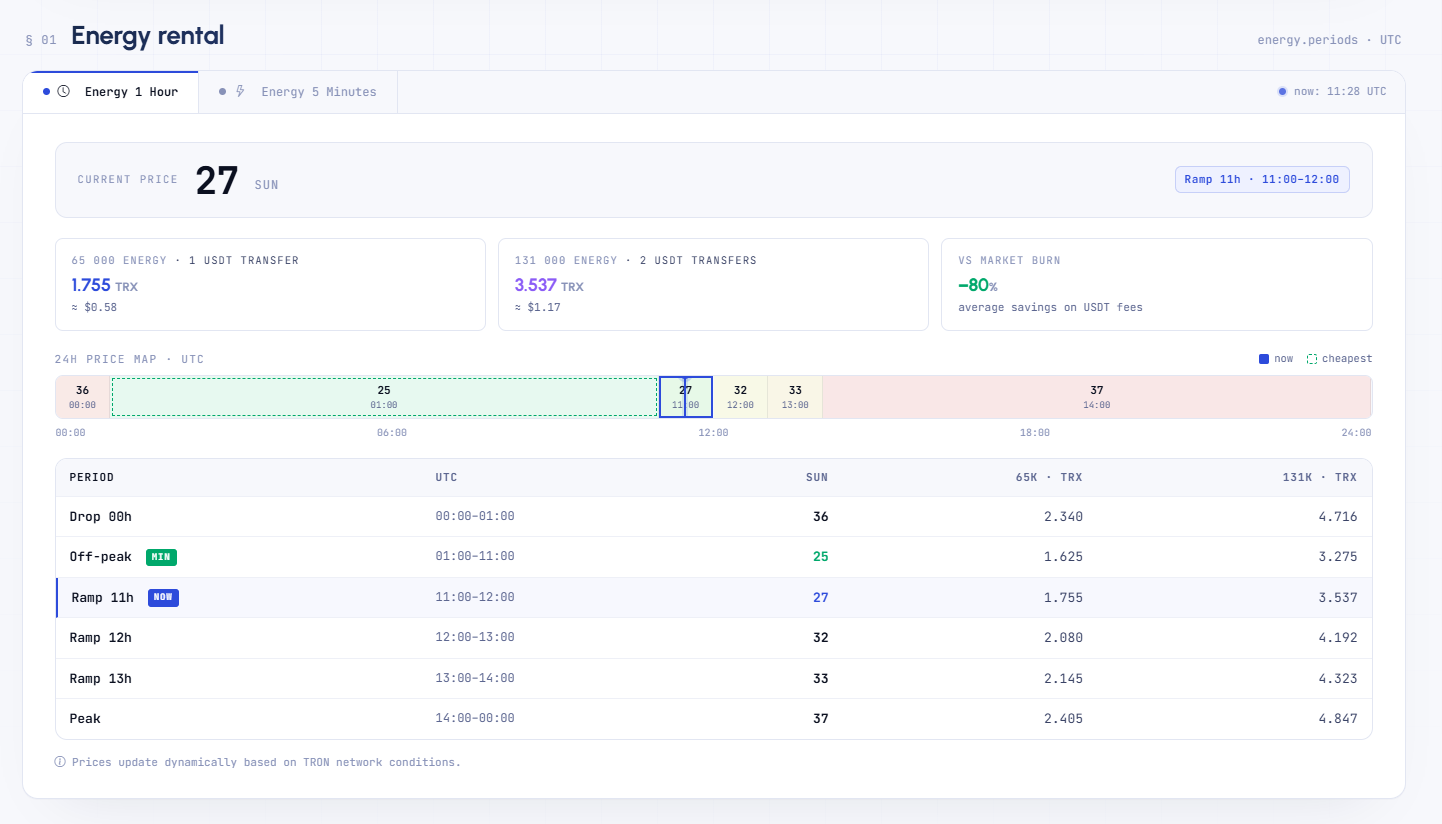

Stablecoins will prove the more indicative data point. USDT alone is responsible for trillions of dollars in settlement each year across all chains, with TRON serving as the global base chain where most high volume USDT transactions take place. It is not for nothing that users prefer stablecoins versus CBDCs, at least in jurisdictions in which both are theoretically available. Outside of a few narrowly-defined national contexts, stablecoins provide the dollar exposure that CBDCs cannot. They work without the surveillance features of CBDCs. They are also usually less expensive to deal with, especially considering that the operational cost of sending USDT efficiently has been reduced by the various Energy management tools developed on TRON to service this exact need. Stablecoins address these pain points more directly than any CBDC in deployment today (USDT users care little about fee structuring or sending transfers cheaply across borders and without intermediation).

It is not unreasonable to make an argument for where CBDCs should get used — wholesale CBDCs as a form of indirect money representing settlements between banks, cross-border payment rails (i.e any of the BIS-coordinated project mBridge work linking central banks in China, the UAE, Thailand, and Hong Kong) or maybe some financial inclusion use cases in truly underbanked jurisdictions. Technically interesting projects with real merit for their very specific use cases. They are also very different from the retail CBDC question, which is the only question that impacts a regular person's relationship with his or her money. The wholesale-retail differentiation is one that is often elided by CBDC proponents and insisted on by critics.

Original vs. Imitation

Whenever something original succeeds in any market, there is a well-established order of events: the imitation will follow shortly thereafter with similar branding and wildly different substance. The simulation is almost always supported by interests that gained from the lack of the authentic and find it easier to compete with a managed version than with the solution that actually addressed the problem. The imitation focuses on the superficial qualities that made the original a hit, and quietly removes all of the structural characteristics that made it valuable. We've all seen this pattern if you've ever bought a discount-store version of a brand name good. CBDCs are a money version of this trend.

The key test isn't how the marketing describes the digital currency; it's which side of that line an instrument falls on between vague crypto impressions and traditional bank instruments. What happens at the edge cases is what defines you. Can the issuer reverse transactions? Can the issuer freeze accounts? Does the issuer have any restrictions how you can spend them? Is it possible for the issuer to restrict transfers, for certain recipients or territories? Is it possible for the issuer to trace all transactions back to a single human? With a CBDC, the answer to all of these questions is yes — and that is written directly in the design documents, even when political messaging tries to definitively state otherwise. In a decentralized cryptocurrency, all of these questions would result in no, and there is ultimately nothing that politics could do to turn the answers into yes, without compromising the fundamental architecture of the network itself.

The two are not equivalent. From a very high level, they fall into the same nominal category — digital currency — and possess a few of the same surface-level attributes, but when you really look into it, nothing else could actually be further apart in substance. This argument has been made over and over again in the crypto community against those pundits who still insist on that analogy. Throughout the argument was right and information from CBDC pilots has tended to assist it. People who want a freedom over their wealth turn to decentralized currencies. Those who want monetary dominance go towards CBDCs. The technologies serve radically different purposes, and pretending otherwise is good debate judo for state-controlled money advocates but has not actually helped illuminate the decision space for the people making it.

If you know what to look for it is not too hard to determine whether the original or an imitation. What it needs is a little commitment not to get stuck just looking at surface features but architectural ones, which is precisely the exercise that separates an actual cryptocurrency from a hundred thousand corporate or governmental things that take the language of “cryptocurrency” and reverse engineer everything substantive. And it always comes down to the same question: who decides what you can do with your money? In the case of a CBDC, the issuer is the source of truth. The answer in a real coin is: you. Everything else is detail.

Netts allows you to purchase Energy exactly when the price is at its lowest and to avoid peaks during rush-hours. Just make sure to discipline yourself to buy low and sell high - and your wallets will thank you!